Key Insights from the 2016 Global Powers of Retailing:

Every January, Deloitte publishes an updated view of the Top 250 largest global retailers. Following is a synopsis of my favorite content from the 2016, 19th edition.

Navigating the New Digital Divide

The Deloitte study “Data suggests there is already a gap between Consumers’ digital behaviors and their local retailers’ ability to deliver the desired experience. We refer to this gap as “the new digital divide,” and it poses a critical challenge to retailers. In order to remain relevant in today’s marketplace, retailers must understand the evolving needs of their customers and improve their ability to anticipate and shape the needs of tomorrow. With more shoppers – both in developed and developing worlds – embracing cultural trends and gaining access to technology that will allow them to be “connected” 100 percent of the time, retailers’ worldwide need to advance their own offerings to fit the behaviors of this new consumer.”

The trends identified lead to three core hypotheses:

- There is no single path towards digital adoption or optimization – Emerging markets are skipping technology adoption phases from developed markets. “The “lift and shift” playbook is likely not appropriate for global expansion.”

- One digital “size” does not fill all customers within a given market – “Consumers clearly use digital tools very differently based on the product type for which they are shopping.”

- Across the world, consumer are demanding digital tools and features to execute their own shopping journey – “Irrespective of culture, digital has a significant impact on in-store retail, and in fact is dramatically more valuable than viewing digital through the lens of online revenue.”

Top 250 Global Retailers Highlights

- Sales-weighted, currency adjusted retail revenue for the top 250 retailers grew 4.3% in 2014. This is on par with the prior year’s 4.1% growth but down from gains posted in 2010 through 2012.

- Retailers in North America and Middle East / Africa had the highest accelerating growth. Asia Pacific, Europe, and Latin America growth decelerated.

- More than half of the top 250 retailers struggled with revenue growth. A quarter had revenue declines. For a third of the retailers, the rate of growth slowed, but remained positive.

- Average net profit margin was 2.8% versus 3.4% the previous year.

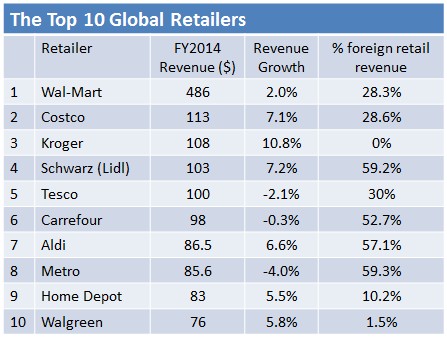

The Top 10 Global Retailers

In the latest Deloitte study, Kroger moved from number 6 to number 3 boosted by multiple acquisitions. Tesco moved ahead of Carrefour purely on the strength of the British pound. Walgreens entered the top 10 replacing Target.

Five of the top 10 global retailers are from the United States and the balance is from Europe. On average, the top 10 retailers had operations in 16.7 countries, ahead of the top 250 average of 10.4 countries.

Retail Product Sector Analysis

- In 2014, the fastest growing retail sector was apparel / accessories. For this sector, revenue increase averaged 6.7% while net profit margin reached 8.1%. Apparel and accessory companies represented 9.7% of total sales for the global top 250 retailers.

- Fast moving consumer goods retailers represent two thirds of the global top 250 retail revenue in 2014. Revenue grew 4.1% and net margin fell to 1.9%.|

- Hardline and leisure goods posted another solid performance in 2014. Top line sales grew on average 6.5% and profitability remained healthy at 3.8%. Sector represents 15.7% of the top 250 global revenues.

The Q Ratio Analysis

A favorite section of the Deloitte report is the annual Q ratio analysis. “The Q ratio is the ratio of a publicly traded company’s market capitalization to the value of its tangible assets. If the ratio is greater than one, it means that financial market participants believe that part of the company’s value comes from its non-tangible assets. These can include such things as brand equity, differentiation, innovation, customer experience, market dominance, customer loyalty, and skillful execution.”

This year, the 10 retailers with the highest Q ratios includes Hermes, Tractor Supply, H&M, Inditex, Amazon, Nike, Next, TJX Companies, Vipshop Holdings, and Ross Stores. The retail format with the highest Q ratio is apparel / accessories, followed by non-store, home improvement, drug store / pharmacy, and discount.

The 2016 Global Powers of Retailing Key Insights

- The digital revolution is just getting started. Sectors or retailers that struggle with brand identity will be challenged through the transformation.

- Emerging markets will not follow linear technology adoption evolution cycles. This is both a challenge and an opportunity for global retail.

- As demonstrated by Kroger, retailers can thrive even in lower margin fast moving consumer goods sectors. Key is strategy execution.

- European retailers are the most international in scope. For Europe, in the latest study, retail revenue growth fell to a five year low as 30% experienced negative growth. Aldi and Schwarz (Lidl) are the model small store exception with both retailers being in the top 10.

- Apparel retailers had the highest percent of retail revenue from foreign operations (31.6%) and are in the most foreign countries (25.9). Is it a coincidence they are also the fastest growing sector?

- Branding will continue to grow in importance, especially in an omnichannel world. Recall the retailers with the highest Q Ratio. “What distinguishes them is the strength of their brands regardless of the channels by which they distribute to consumers.”

Welcome to the disruptive future of retail where the focus needs to be on delivering continuously immersive positive digital customer experiences.

For additional retail, technology, and leadership information visit www.tonydonofrio.com

Article by channel:

Everything you need to know about Digital Transformation

The best articles, news and events direct to your inbox

Read more articles tagged: Featured, Operating Model